The landscape of the stock market has transformed significantly over the last few decades. What used to involve physical certificates and manual paperwork is now handled entirely through digital

-

-

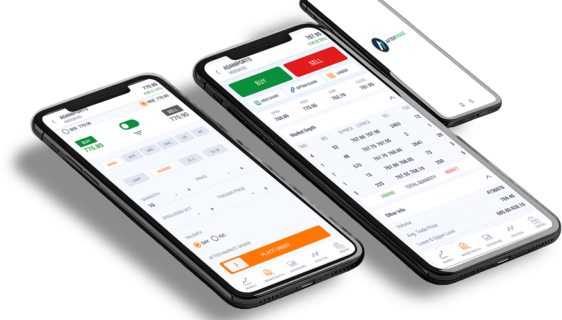

Financial markets offer a wide range of opportunities, but not every trading method appeals to investors who prefer a fast-paced and flexible approach. Active traders, in particular, look for tools

-

On a big construction job, steel plates are not an afterthought; they decide how loads move, how joints behave, and how well the structure stays aligned during erection. When plates are

-

The digital age has changed how we handle our finances. It is now possible to apply for credit while sitting on your couch or waiting for a coffee. This convenience has made it easier for people to

-

Buying a rear loader garbage truck is a major investment for municipalities, waste management companies, and private contractors. Understanding the price and ongoing costs helps planners make smart

-

The digital marketing landscape has undergone a seismic shift over the last decade, moving away from traditional broadcast advertisements toward the more personal and nuanced world of social proof.

-

The digital media landscape is rapidly evolving. Audiences expect content to be accessible across websites, mobile apps, social media, and even connected devices. To meet these demands, media

-

Ever found yourself in a bit of a financial pickle, and wondered how to get out of it quickly? That's where instant personal loans come in, offering a lifeline when you need it the most. The beauty

-

Businesses can grow quickly with paid media. This encompasses online ads such as Google Ads, Facebook ads, Instagram promotions, YouTube ads and sponsored content. When created effectively,

-

EIC Accelerator is one of the most competitive innovation funding instruments in the world, with overall success rates typically in the mid single digits. For CFOs and founders, understanding why